Table of Content

A higher loan amount will mean a higher monthly mortgage payment. Borrowing too much could make it difficult to ride unexpected financial bumps, such as a job loss or a big medical bill. Lenders will look at your payment history, income, and current debts to determine how likely you are to pay your loan each month. The number value assigned to your “reliability” is known as your credit score and is one of the biggest factors in getting approved for a mortgage. By seeking preapproval before landing on a home, borrowers can uncover, resolve or avoid these adverse issues before the mortgage process moves forward. With the knowledge of how much you’ll be able to borrow, you can explore buying options with the certainty that the property is in your price range.

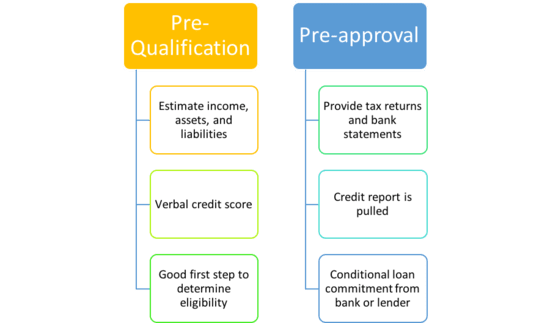

After that, you’ll need to apply again with another credit pull and updated paperwork. If there are any major changes to your financial situation, your preapproval limit might also change. A mortgage prequalification signifies that a mortgage lender has collected some basic financial information about you, and sometimes completed a credit check, to estimate how much house you can afford. This process is less formal than preapproval and, when completed online, can yield a response immediately—though some lenders take longer.

Mortgage Calculators

It can be the first step of your home-buying process and an opportunity to shop around and compare loan offers. Preapproval,” involves providing documentation of everything you reported in your pre-qualification and a hard credit pull. Preapproval demonstrates a more serious step towards homeownership, whereas pre-qualification is an optional process that can be helpful for understanding your financial readiness to buy a home.

It also makes the mortgage application process that much smoother. Some lenders base preapproval letters solely on the information you provide. Other lenders dig into the details with you now to make certain you have all the documentation you need and prevent delays and surprises later. All lenders will require documentation at some point if you decide to apply for a loan.

Preapproval vs. prequalification: What’s the difference?

Offers full online mortgage application, rate quotes, document upload and loan tracking. When kicking off your home search, understanding a realistic purchase price is critical. Otherwise, you could start your search looking for homes well above what you can realistically afford. It’s important to note that a prequalification offer is not binding. Instead, it’s subject to a further review of your financial details.

Before you start looking for your first home, we can help you with a mortgage prequalification. NSB offers payment processing solutions to fit the needs of all business types. Decrease your overall debt to improve your debt-to-income ratio. Typically, a debt-to-income ratio of 36 percent or less is preferable; 43 percent is the maximum ratio allowed. Use ourdebt-to-income calculatorto estimate your debt-to-income ratio.

How to increase your prequalification amount

However, because prequalification doesn’t involve an in-depth review of borrower finances, it does not guarantee you’ll be approved for a mortgage. If you’re in the market for a new home, you can request a mortgage prequalification at your local bank branch or—in many cases—online. However, lenders also use prequalifications as a marketing tool by targeting creditworthy borrowers who they suspect are potentially low-risk mortgage customers. These offers typically come in the form of phone calls or mail and may include preliminary mortgage details.

To document the loan prequalification, the homebuyer receives a special letter from the lending institution or loan officer. A loan prequalification can aid a homebuyer in the purchase of a home because it gives the buyer a clearer picture of how much money can be spent toward the purchase of the home. As a buyer with loan prequalification, the homebuyer has the option of negotiating a better price or a reasonable payment plan with the seller. Mortgage preapproval is the process of determining how much money you can borrow to buy a home. Lenders such as Rocket Mortgage® look at your income, assets and credit score and determine what loans you could be approved for, how much you can borrow and what your interest rate might be.

Mortgage prequalification involves getting an estimate of how much your lender may be willing to lend based on your general creditworthiness. All of your monthly payments toward your existing and future debts should usually be less than 43% of your monthly income. However, the amount you qualify for based on this calculation may not be suitable for you. You should review your personal situation and work with a financial advisor to decide how much you can comfortably afford. To calculate your debt-to-income ratio, divide your monthly payments by your monthly gross income. When you prequalify for a home refinance with multiple lenders, you’ll be able to compare loan options and interest rates, along with fees for appraisal, origination, and other closing costs.

Although not a binding loan offer, a prequalification is very useful for home shoppers. The amount outlined in the letter can help you determine a realistic budget for your future home. With a prequalification, you’ll understand how much house you can actually afford based on your savings, credit score, and today’s interest rates.

The rate and loan amount you’re offered aren’t binding until you’ve completed a full loan application and submitted all your financial documents. The lender’s underwriting process will verify your eligibility, rate, and loan size. Keep in mind that a home’s purchase price isn’t the only thing that impacts affordability. Your mortgage rate also plays a big role in determining how much house you can afford and what your monthly mortgage payment will be.

Estimated monthly payment and APR calculation are based on a down payment of 3.5% and borrower-paid finance charges of 0.862% of the base loan amount. Estimated monthly payment and APR assumes that the upfront mortgage insurance premium of $4,644 is financed into the loan amount. The estimated monthly payment shown here does not include the FHA-required monthly mortgage insurance premium, taxes and insurance premiums, and the actual payment obligation will be greater.

Annual percentage rate represents the true yearly cost of your loan, including any fees or costs in addition to the actual interest you pay to the lender. The APR may be increased after the closing date for adjustable-rate mortgage loans. Mortgage pre-qualification is an informal evaluation of your creditworthiness and how much home you can afford based on self-reported information like your credit, debt, income and assets. Based on these inputs, pre-qualification estimates the amount a lender may be willing to lend you. Check your credit score, which is a number between 300 and 850. A higher score not only improves your chances of getting a mortgage loan, but may also help you qualify for a lower interest rate.

No comments:

Post a Comment